Global Economy – 2026 Outlook

Table of Contents

-

-

- 2025 was a year of high volatility yet characterized by an upward trend

- The Economy in 2025

- USA

- Europe

- Emerging Markets

- China

- Japan

- Greece

- The Fixed Income Market

- Alternative Investments

- Cryptocurrencie

- 2026 Outlook

- Disclaimer

2025 was a year of high volatility, yet characterized by an upward trend

2025 was a year of remarkable resili-ence for the global economy and markets, despite intense geopolitical pressures and trade uncertainties.

Global Economy

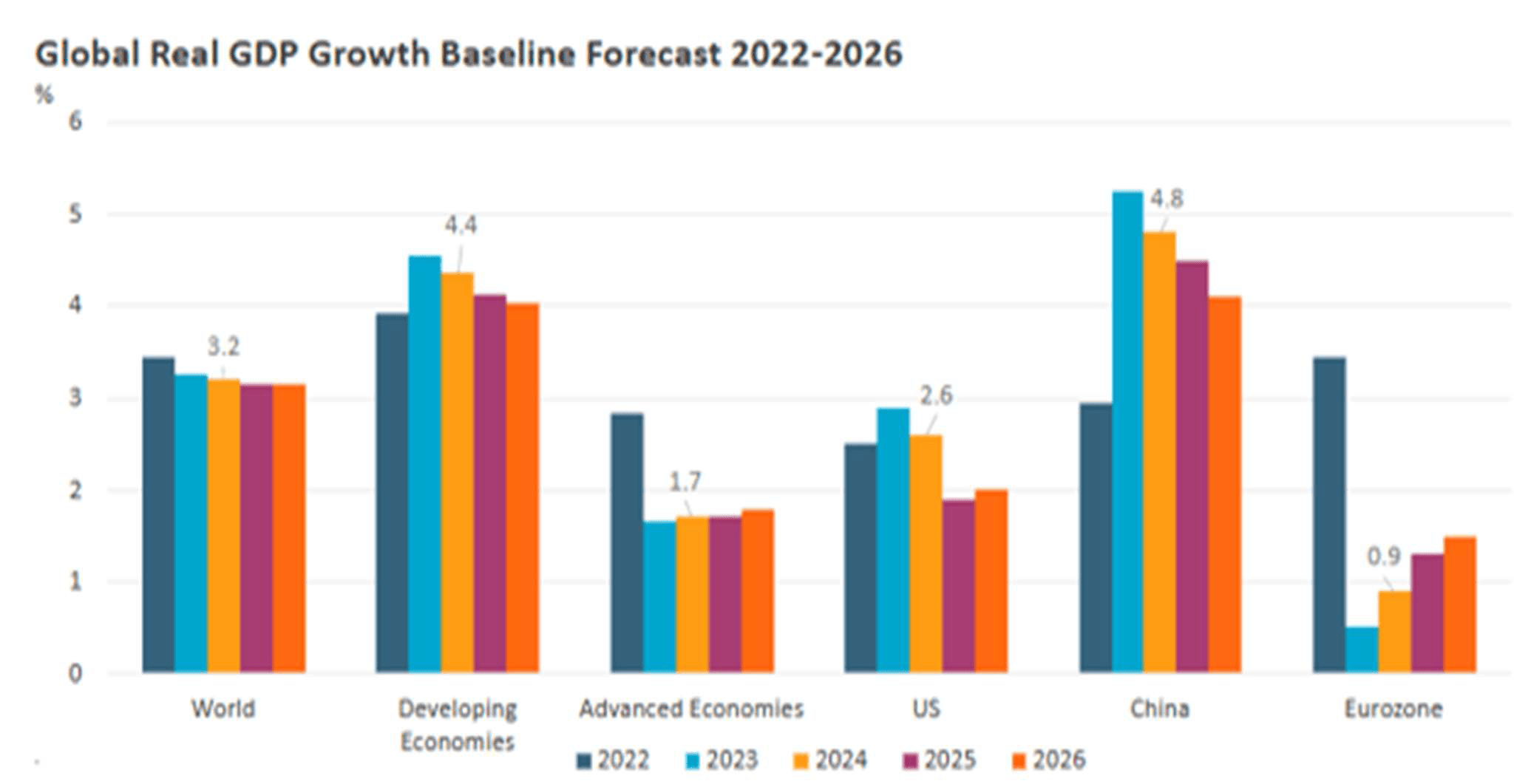

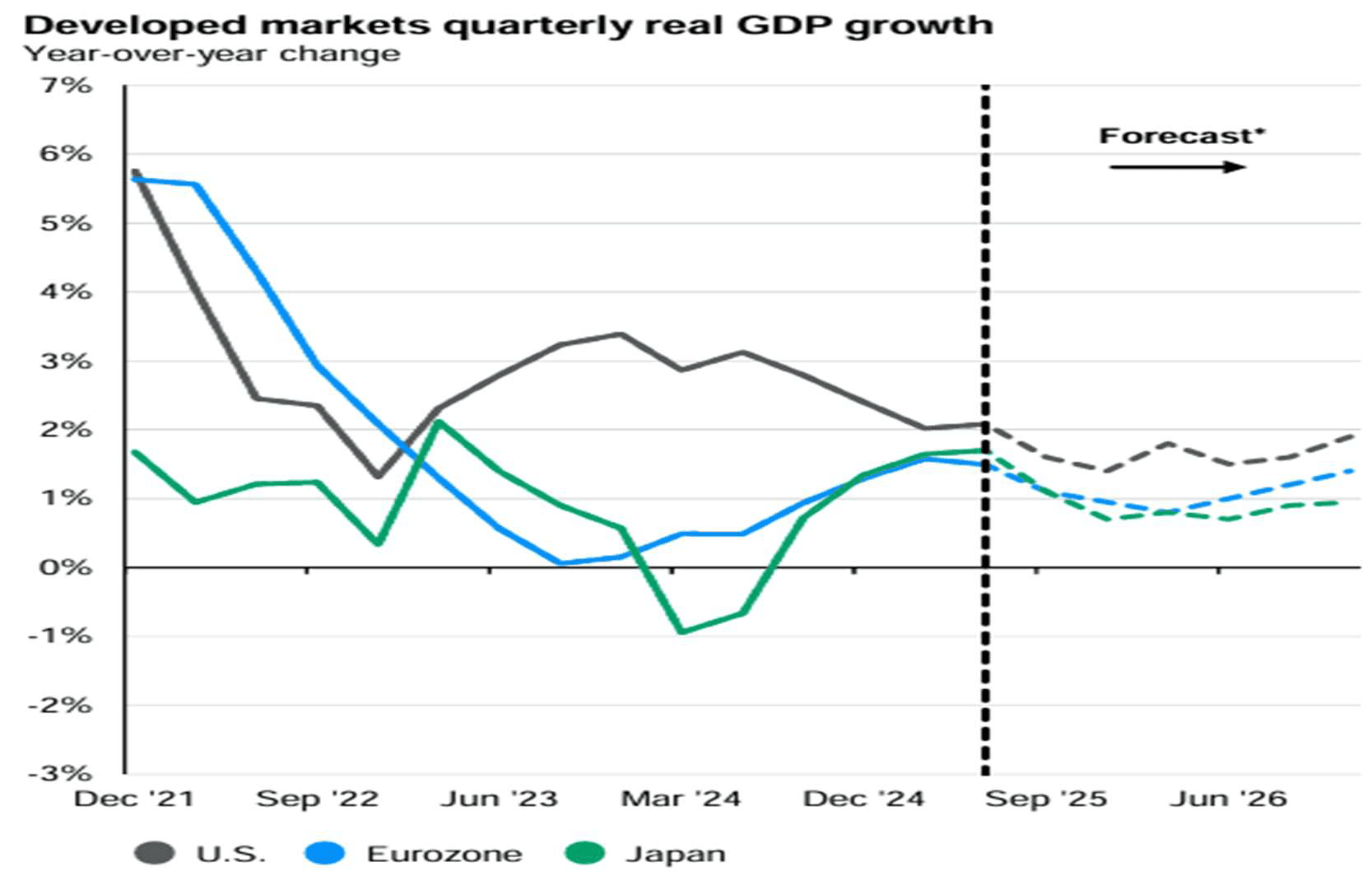

Global GDP is estimated to have grown at a rate of 3.2%. Growth in matured economies hovered around 1.5%, while emerging mar-kets displayed stronger momentum, exceed-ing 4%.

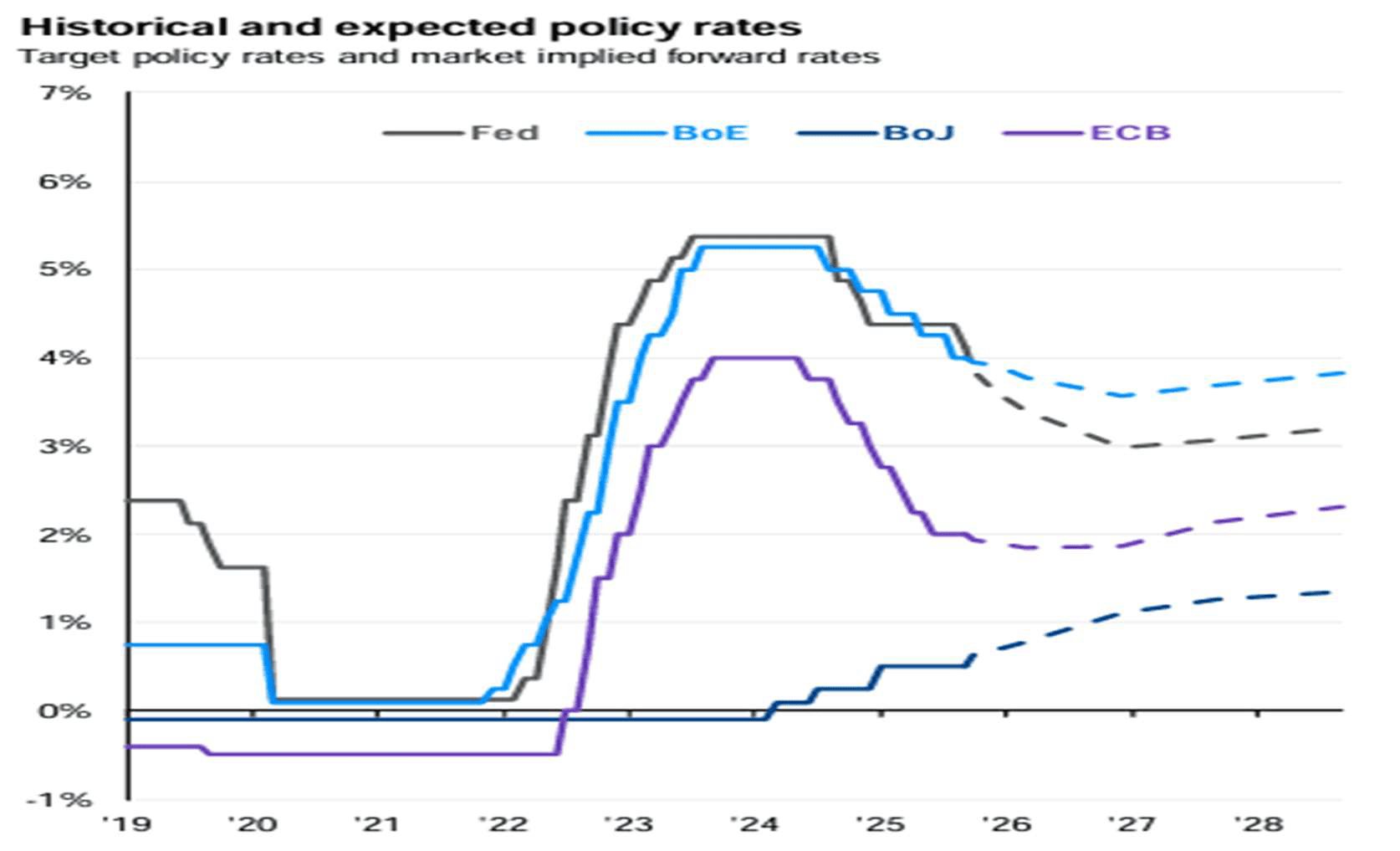

Inflation and Interest Rates: Inflation contin-ued its downward trajectory globally, allowing central banks (such as the Fed) to maintain the interest rate-cutting cycle, although in the US, it remained slightly above target.

The year was marked by tariff increases and trade tensions, which, however, did not trig-ger the sharp recession that markets had feared at the beginning of the year.”

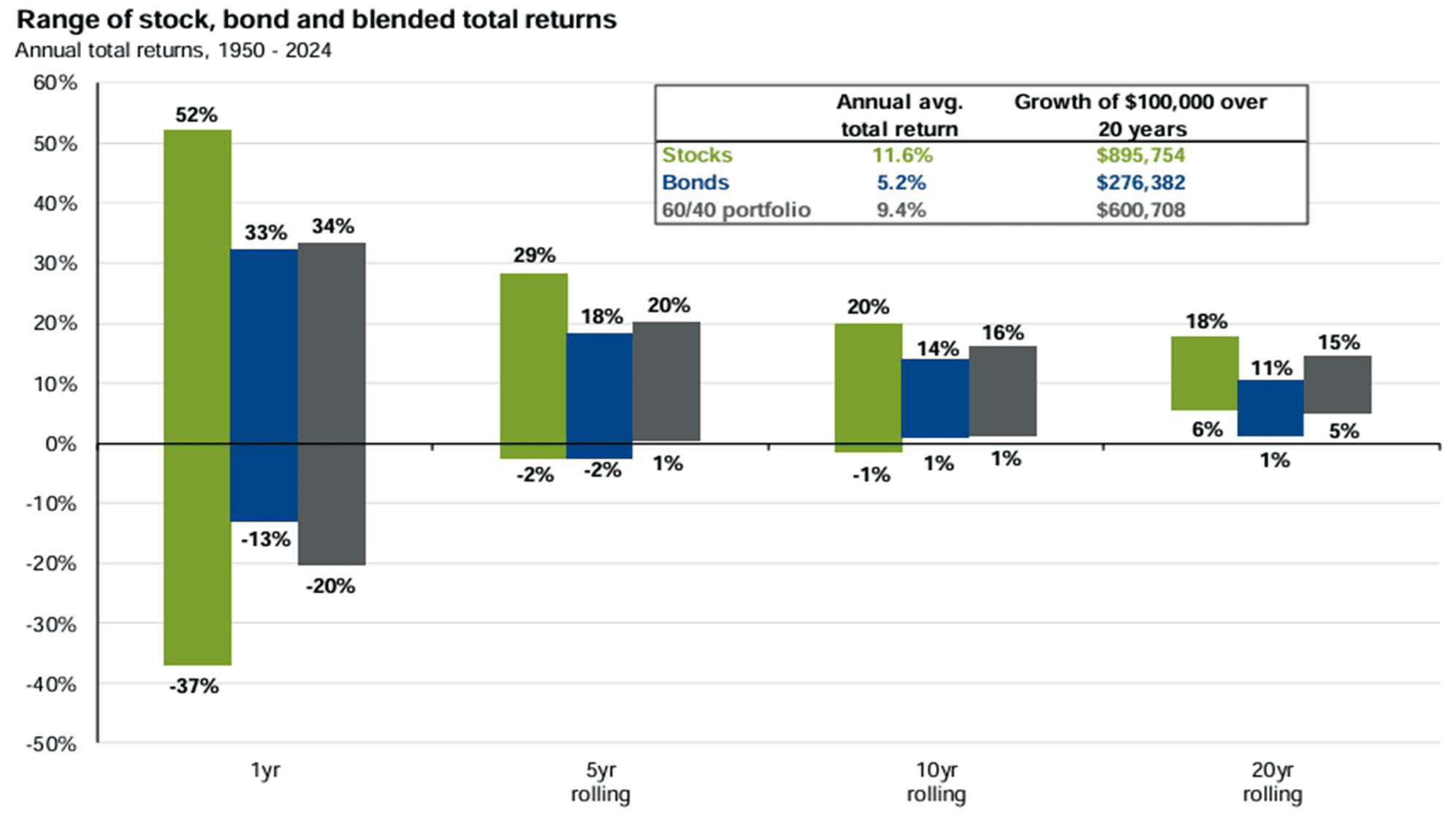

2025 was an exceptional year for equities, with many markets recording double-digit gains. In the US, the S&P 500 rose by approx-imately 17-18%, reaching all-time highs in December, while in Europe, the German DAX climbed by 22%, and Japan’s Nikkei recorded an impressive 29% surge. Emerging Markets made a strong comeback with year-to-date gains of nearly 25%. Artificial Intelligence (AI) remained the primary growth driver, with technology and semiconductor stocks (such as Micron and Western Digital) delivering the highest returns.

In Greece, the Athens Stock Exchange stood out internationally, recording the fifth-highest performance globally for 2025, while the Greek economy grew at a rate of 2%, outper-forming the Eurozone average.

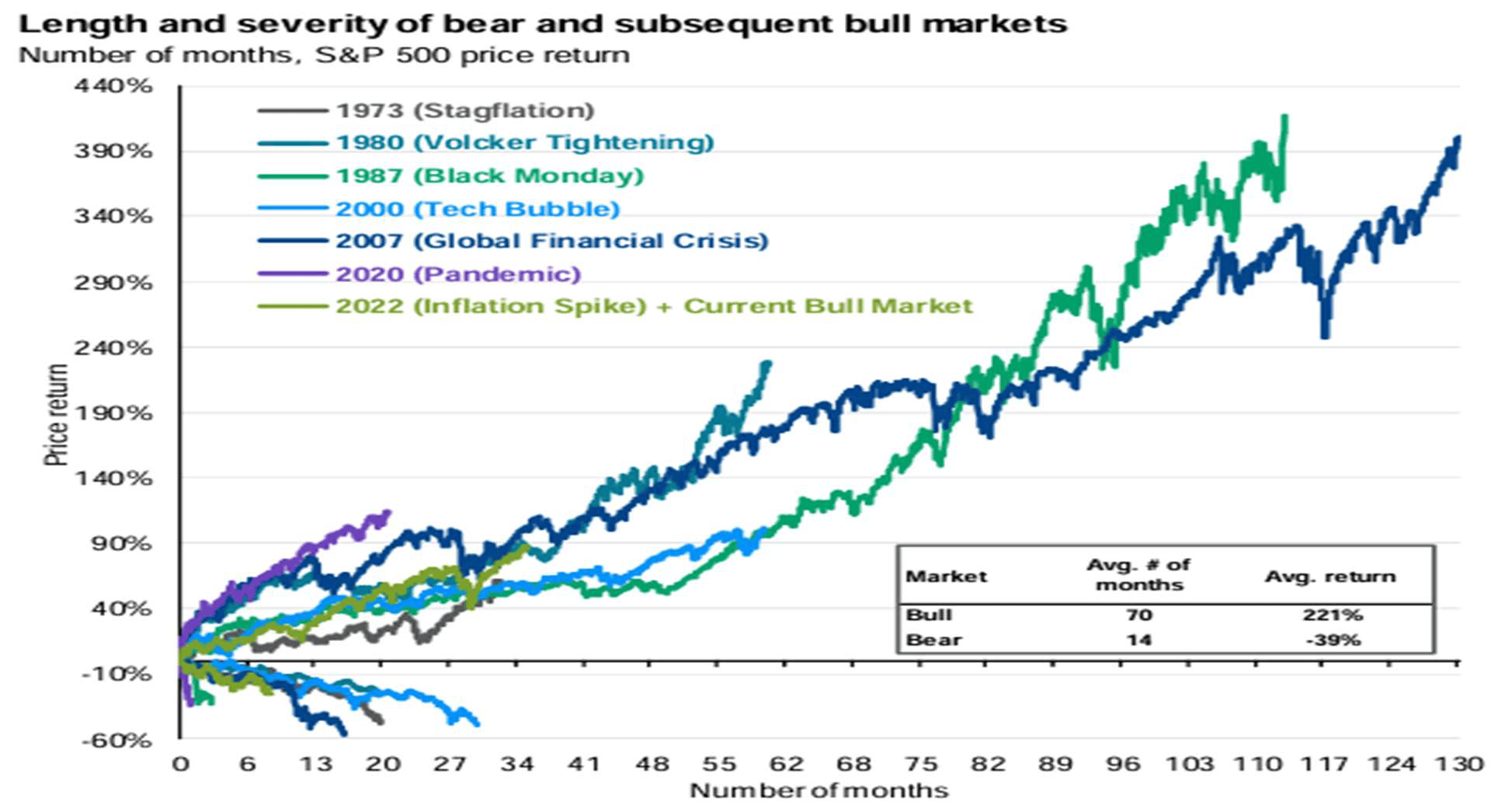

In commodities and precious metals, gold acted as the ultimate ‘safe haven’, though it exhibited significant volatility due to geopolit-ical unrest. Despite this positive trajectory, the year closed with concerns regarding the sustainability of growth in 2026, due to ele-vated public debt and tariff policies. Overall, global economic growth has exceeded expec-tations this year, in some cases by a signifi-cant margin. As growth maintained its up-ward momentum, expectations grew that it was ‘nearing its peak’ due to geopolitical de-velopments and that a reversal was highly likely. However, this remained theoretical, as actual returns eventually defied bearish sce-narios. Valuations remain high, as do expec-tations for further growth, which is funda-mentally driven by technology and its trans-formative impact across various sectors.

The investor preference for equities over oth-er major asset classes (such as bonds) is ex-pected to persist among consumers, given the outlook for their performance.

Regarding cryptocurrencies, despite the ‘cryp-to winter’ observed towards the end of the year, the total market capitalization of the cryptocurrency market surpassed $4 trillion for the first time within 2025, confirming the industry’s maturation. 2025 served as a mile-stone year, as the cryptocurrency market moved decisively from the fringes to the fi-nancial mainstream. Even in Greece, under Law 5193/2025, crypto-assets were officially recognized as investment tools and financial instruments by the Ministry of Finance.

-

The Economy in 2025

The beginning of 2025 found the world facing five key expectations from international fi-nancial institutions regarding upcoming polit-ical and economic developments.

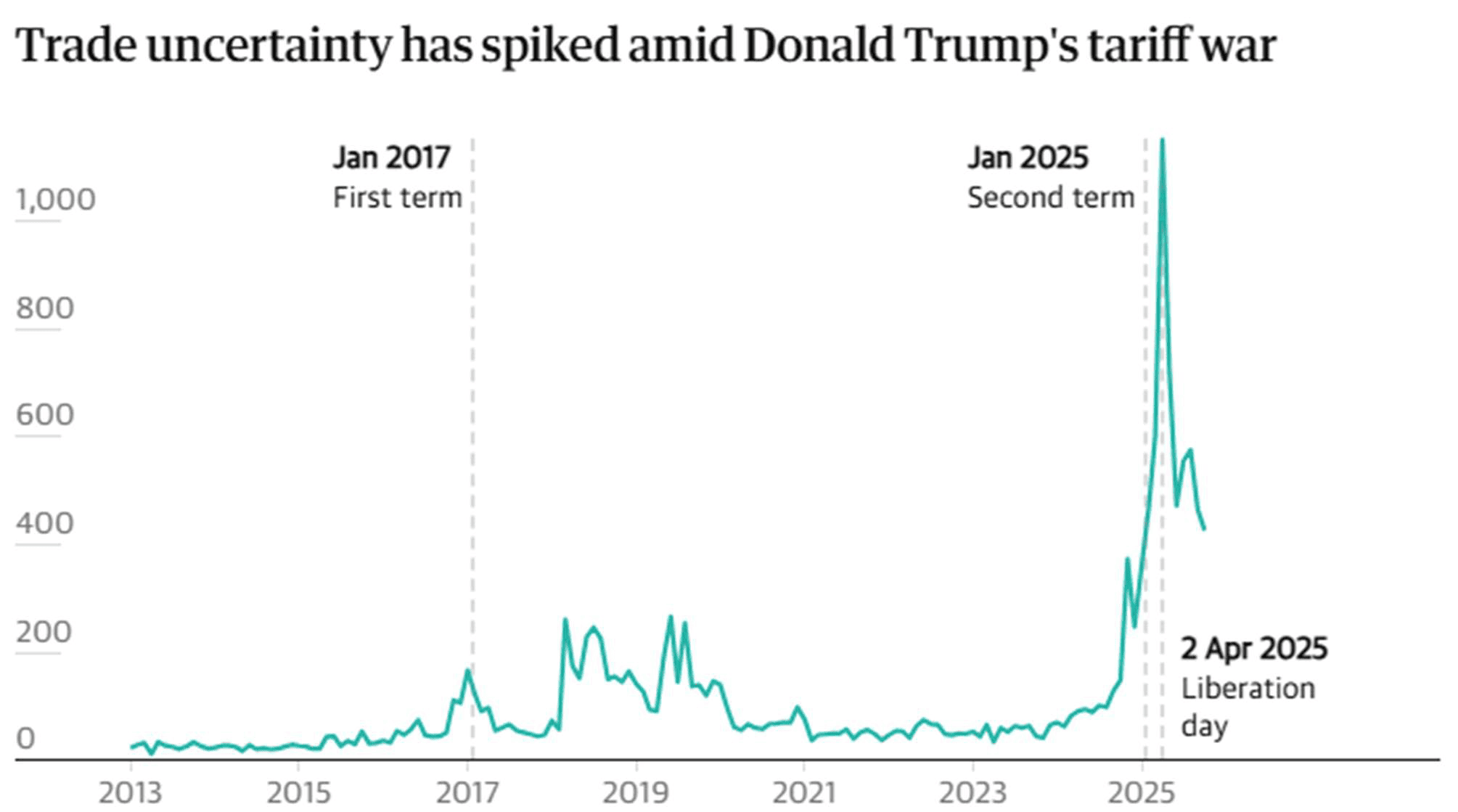

The first was the return of Donald Trump to the White House, which not only materialized but also led to shifts in tariffs (the second ex-pectation), triggering a trade war with coun-tries such as China and the European Union, as well as other emerging markets. This caused significant market disruptions, as companies were compelled to seek alterna-tive markets to avoid the ‘tariff trap’. The turmoil was such, that it severely strained economies, particularly in the first half of the year, and provoked sharp rhetoric from all sides, creating an unfriendly and, above all, erratic environment for assessing risks and identifying investment horizons.

Source: Euromonitor International Macro Model

The third expectation concerned the migra-tion issue, which remained a central focus throughout 2025 and will continue to be, as flows from Africa and Asia to Europe are not subsiding; on the contrary, they are creating challenges of immense proportions. The pri-mary concerns involve housing and employ-ment for millions of migrants, including those arriving for studies (student housing has now become an endangered commodity) and those seeking to settle permanently for a bet-ter and more promising future.

The fourth expectation involved the wars in the Middle East and Ukraine-Russia. With a toll of numerous casualties and widespread homelessness and poverty, the conflicts per-sisted for most of the year, with occasional glimmers of hope as the US President took initiatives on both fronts. While peace seemed momentarily possible, the situation (especially regarding Ukraine) eventually re-verted to a state of sustained warfare. In the Middle East, however, the landscape is dif-ferent, with history suggesting that a cease-fire is closer to achieving a peace treaty and a final agreement.

Finally, the fifth expectation was the further flour-ishing of Artificial Intelligence. This not only mate-rialized but has become a new expectation for 2026: to continue its leap-frog growth and the rapid changes it has already begun to bring to our lives.

-

USA

The global economy suffered a major shock last April when the Donald Trump admin-istration adopted an aggressive tariff policy aimed at trade restructuring and narrowing U.S. deficits. This move triggered intense market uncertainty and forced businesses to overhaul their supply chains.

Despite the bilateral agreements that fol-lowed, U.S. tariff rates surged from 2.5% (at the start of 2025) to 17.9%. According to Yale University’s Budget Lab, these are the highest levels recorded since 1934.

2026 is considered a milestone year, as the U.S. Supreme Court is set to rule on whether the President is legally authorized to impose tariffs by bypassing Congress under the pre-text of ‘national emergency.’ Although many analysts predict a judicial strike-down of these measures, it is estimated that the ad-ministration will seek alternative legal ‘loop-holes’ to maintain them, keeping the issue high on the agenda.

Source: JPMorgan – A Guide to the Markets

On the front of Sino-American relations, the meeting between Trump and Xi Jinping in Busan led to a temporary one-year truce. However, this calm is only superficial. The profound geostrategic competition in cutting-edge sectors—such as Artificial Intelligence, robotics, and defense technology—foreshadows a new cycle of sanctions and countermeasures in the future.

Source: JPMorgan A Guide to the Markets

Disinflation gets back on track

Source: Haver Analytics, Goldman Sachs Global Investment Research

-

Europe

In 2025, the European economy demonstrat-ed remarkable resilience despite geopolitical challenges, while for 2026, the outlook re-mains cautiously optimistic, with an emphasis on stability.

In 2025, growth exceeded expectations. Spe-cifically, EU GDP grew at a rate of 1.4% (re-vised upward from 1.1%) and the Eurozone GDP at 1.3%. This performance was primarily driven by a surge in exports to the US, as companies rushed to front-run the imposition of Trump tariffs, as well as by strong invest-ments in equipment. Spain stood out with a growth rate of 2.9%, while France moved at 0.7%, and Germany remained nearly stag-nant at just 0.2%. Greece maintained a posi-tive growth rate of approximately 2.1%. Re-garding inflation, the downward trend con-tinued, receding to 2.1% in the Eurozone, ap-proaching the European Central Bank’s (ECB) target.For 2026, there is a growth momentum that is, however, quite sluggish and restrained. Growth in the EU is projected to remain at 1.4%, while the Eurozone is expected to see a slight deceleration to 1.2%. The main pillars of growth will be public spending—with an ex-pected increase in defense expenditures and infrastructure investments (notably in Ger-many)—and consumption, where recovering real wages and lower interest rates are ex-pected to boost household spending, although consumer confidence remains fragile.

In the Old Continent, risks and challenges continue to include trade tensions, such as US tariffs which could shave off up to 1% of EU growth by the end of 2026, and fiscal sta-bility, as many countries will be called to bal-ance increased spending with the need for fiscal consolidation due to high debt levels.

In the labor market, unemployment is pro-jected to hit a historic low (5.7% in the EU), a very positive outlook, yet labor shortages and demographic pressures will slow down the creation of new jobs.

Overall, in 2026, Europe must navigate a shifting global trade environment, focusing on enhancing competitiveness and economic security.

Source: JPMorgan – A Guide to the Markets

-

Emerging Markets

Emerging Markets (EM) significantly outper-formed the U.S. and other major markets this year.

Emerging markets displayed robust economic performance in 2025, and the outlook for 2026 remains favorable, with developing economies serving as the engine of global growth. 2025 was an exceptional year for emerging markets, which recorded substan-tial gains and outpaced advanced economies. The overall GDP growth rate in emerging economies reached 4.1%, maintaining a sig-nificant lead over advanced economies (ap-proximately 1.5%).Emerging market equities returned nearly 30% in dollar terms during the first 11 months of the year, despite geopolitical tensions. Ex-ports were less affected by U.S. tariffs than anticipated, as global trade rebounded.

For 2026, growth is expected to remain strong, albeit slightly decelerating. GDP growth is projected to remain near 2025 lev-els, at approximately 4.1%, with Asian econo-mies leading the way. Technology and AI-related exports are expected to continue their upward trajectory, primarily benefiting Asian markets such as Taiwan and South Korea.

Lower global interest rates and domestic monetary incentives are expected to further stimulate markets. Long-term trends, such as demographics, urbanization, and institutional reforms, are expected to continue supporting growth.

Finally, the impact of increased U.S. tariffs is expected to be more pronounced in non-tech exports in 2026, while political uncertainty remains a risk factor. Overall, emerging mar-kets are expected to maintain their positive trajectory, benefiting from internal dynamics and technological progress.

-

China

The Chinese economy demonstrated remark-able momentum in 2025 despite external pressures, while for 2026 it is preparing for a cautious transition with an emphasis on do-mestic stimulus. The country appears to be meeting its 2025 growth target, with GDP ex-pected to close with an increase of approxi-mately 5%. Goldman Sachs, in fact, revised its estimates upward due to robust exports.

Despite the trade war with the US, the coun-try’s annual trade surplus exceeded $1 trillion for the first time, as Beijing channeled its products into new markets, such as Central Asia. Despite overall growth, the economy was impacted by the persistent crisis in the real estate sector, limited domestic demand, and a decline in private investment.

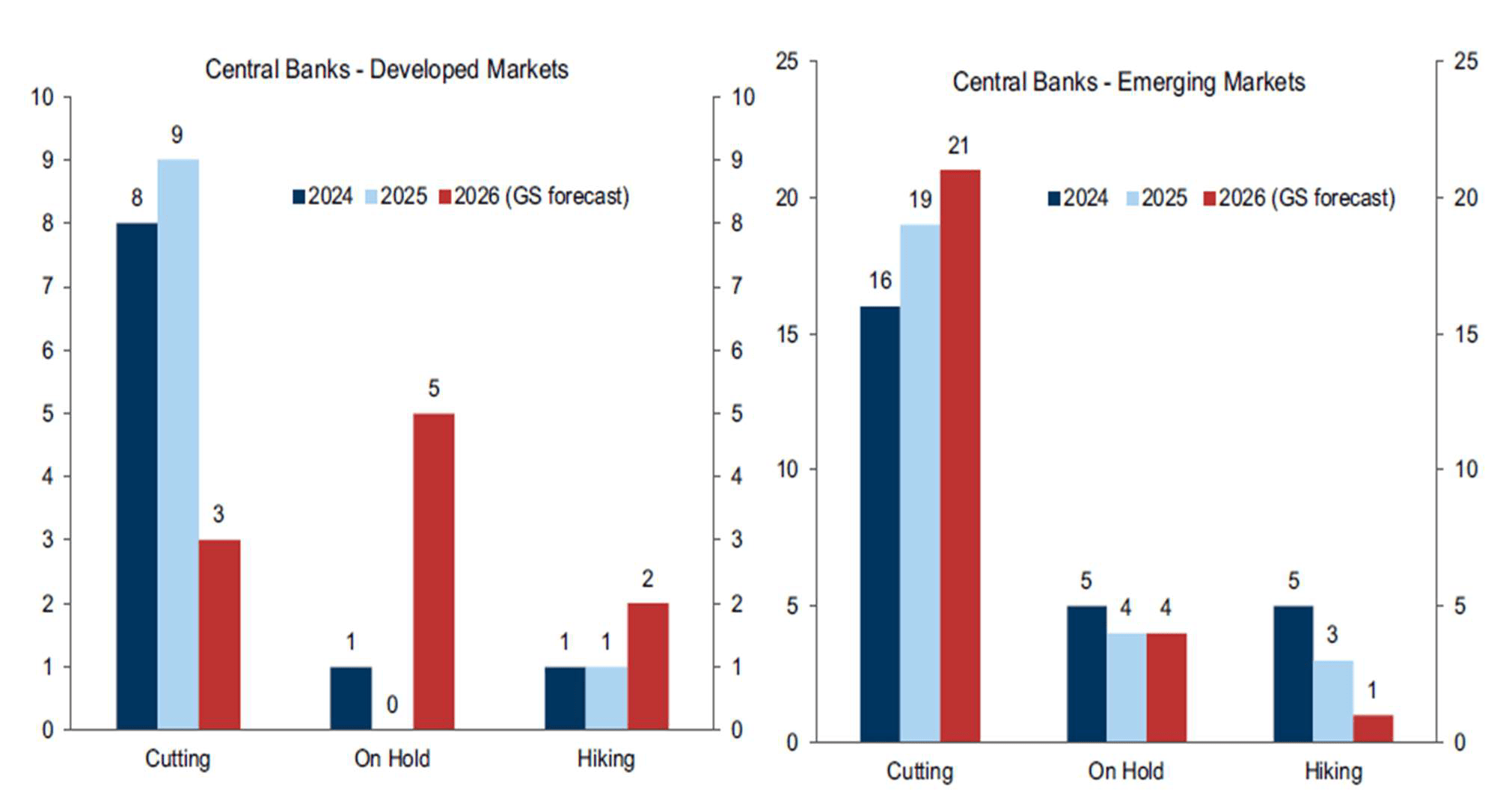

2025 was a strong year for Chinese equities, with the A-share index reaching a decade high and Hong Kong reclaiming its position as a leading market for IPOs. For 2026, interna-tional organizations (IMF, World Bank) pre-dict a slight dip in the growth rate, estimated to move between 4.2% and 4.5%. The Chi-nese government has set the strengthening of domestic consumption as an absolute pri-ority for 2026 to offset losses from foreign trade. Beijing is expected to maintain an ele-vated fiscal deficit (around 4% of GDP) to support local governments and finance new infrastructure projects.More differentiation in central bank cycles in 2026, but still skewed to lower policy rates

Source: Haver Analytics, Goldman Sachs Global Investment Research

The primary threats remain geopolitical ten-sions with the West, the risk of deflation, and demographic pressures. In summary, China is expected to pursue ‘high-quality growth’ in 2026, attempting to reduce its reliance on ex-ports and lean more heavily on domestic de-mand and technological innovation.

-

Japan

In 2025, Japan stood at a historic turning point for its monetary policy, while the new year is expected to be one of stabilization with an emphasis on domestic consumption. The Japanese economy grew at a rate of approxi-mately 1.1% to 1.3% for the 2025 fiscal year. Despite its resilience, the year was marked by challenges, such as the imposition of 15% tar-iffs by the US on Japanese exports in Sep-tember, which caused a temporary GDP con-traction in the third quarter.

The Bank of Japan (BoJ) proceeded with his-toric interest rate hikes, reaching 0.75% in December 2025—the highest level in 30 years—signaling the end of zero-interest rates. This move was aimed at curbing infla-tion and supporting the yen. Inflation re-mained persistently above the 2% target, hit-ting 3% in November. However, wage in-creases during the spring negotiations (Shunto) were the highest in decades, ex-ceeding 4%. The depreciation of the yen led to record-breaking international tourist arri-vals, significantly boosting service sector rev-enues.

Source: JPMorgan – A Guide to the Markets

The government projects a growth rate of 1.3% for fiscal year 2026 (starting in April), betting on a recovery in private consumption. Conversely, international organizations such as the OECD are more conservative, forecast-ing growth near 0.9% due to the impact of tariffs. Further interest rate hikes are ex-pected from the BoJ, potentially reaching 1.0% or higher, as inflation shifts from ‘cost-push’ to ‘demand-pull.’ The new administra-tion of Sanae Takaichi approved a record-breaking budget of 122.3 trillion yen (€665 billion) for 2026, with an emphasis on de-fense, social welfare, and investment stimu-lus.

The primary risks for 2026 include a potential deterioration in Japan-China relations, sharp fluctuations in the yen, and labor shortages due to demographic aging. In 2026, Japan will seek to fully normalize its economy, leav-ing behind decades of deflation while simul-taneously managing pressures from the in-ternational trade environment.

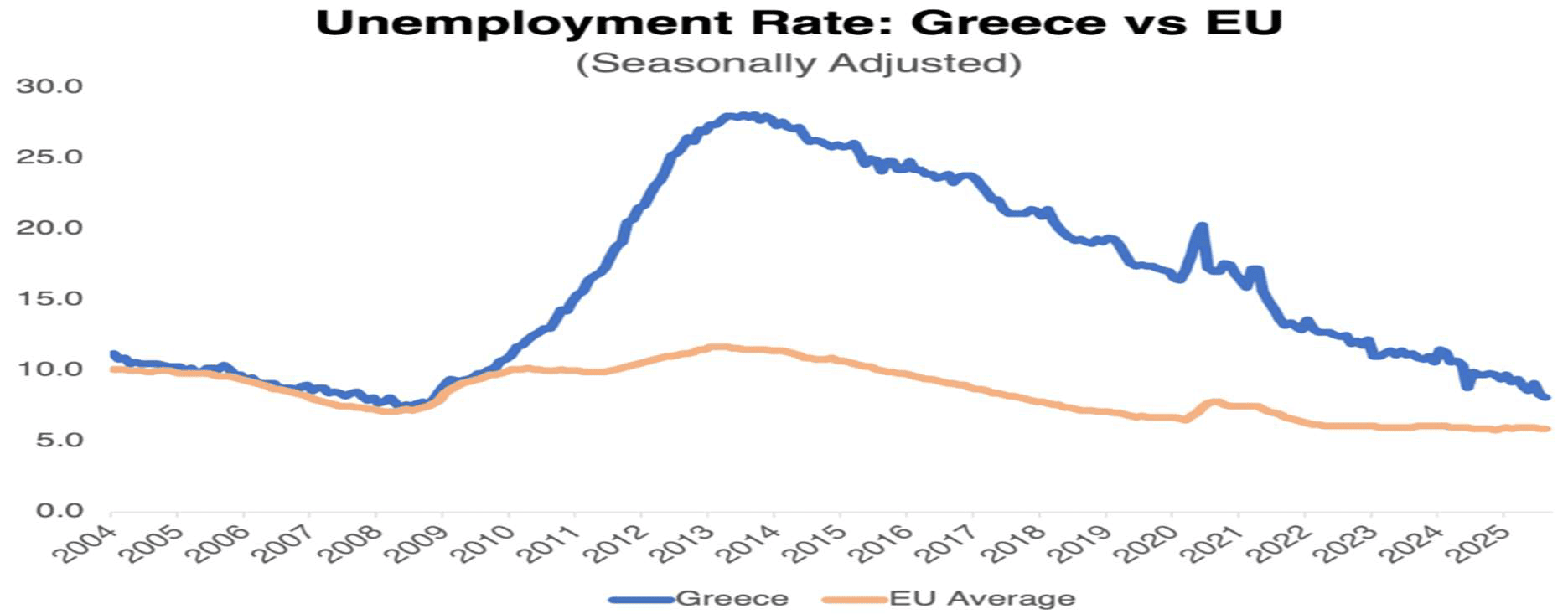

- Greece

In 2025, the Greek economy demonstrated remarkable resilience, maintaining growth rates consistently above the Eurozone aver-age, with forecasts for 2026 remaining posi-tive despite international uncertainties.

Growth is estimated at 2.1% – 2.3%, driven primarily by private consumption and invest-ments, which reached a 15-year high at 16.6% of GDP in the second quarter. Tourism con-tinued its role as the “locomotive” of the economy, with travel receipts increasing by 9% year-on-year during the first nine months.

Source: IMF

Greece achieved a historic primary surplus reaching 4.8% of GDP (based on 2024 data impacting 2025), allowing for the provision of permanent social support measures amount-ing to €1 billion. Unemployment retreated to a 17-year low, hitting 8.0% in July. Wages in-creased by an average of 3.6%, driven by the rise in the minimum wage and reductions in social security contributions. Inflation re-mained at 2.8% – 2.9%, primarily due to food and services prices.

The stock market delivered a record return of over 40%, outperforming all European and other organized markets, following its official reclassification as a ‘developed market’ from ’emerging’ after years of being downgraded. The acquisition of EXAE (Hellenic Exchang-es) by Euronext serves as compelling evi-dence of the significant upgrade in technology and services within a competitive environ-ment; however, this development is expected to impact Greek brokerage firms (particularly private ones).

Source: Eurostat

For 2026, growth is expected to accelerate or stabilize at 2.2%. The full implementation of the Recovery and Resilience Facility (RRF) is projected to add a total of 7% to real GDP by the end of the year. Regarding public debt, a further de-escalation to 142.1% of GDP is an-ticipated. Greece plans the early repayment of bilateral loans amounting to €8 billion within the 2026-2028 period. For 2026, a relief package has been announced (costing 0.6% of GDP), which includes reductions in income tax, ENFIA (property tax), and VAT, as well as pension increases, while inflation is ex-pected to significantly de-escalate toward 2.1% – 2.3%.

Despite the positive outlook, the economy faces risks from the international environ-ment, such as geopolitical tensions and po-tential impacts from tariffs on international trade. Demographics and the housing crisis are emerging as significant medium-term challenges for the country.

-

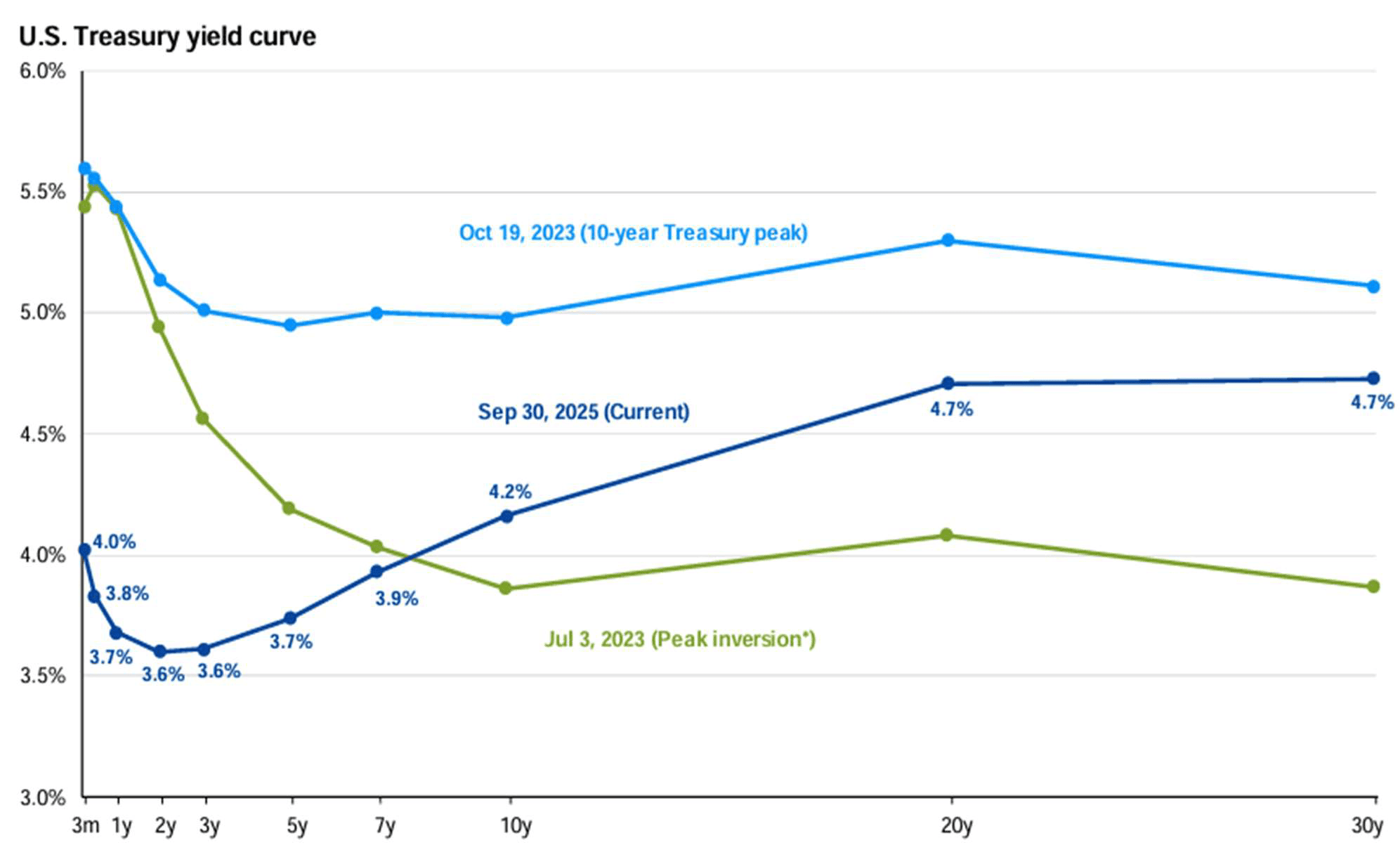

The Fixed Income Market

The bond market in 2025 was characterized by intense volatility and regional divergences, while 2026 is expected to be a year of ad-justment to new fiscal and monetary realities.

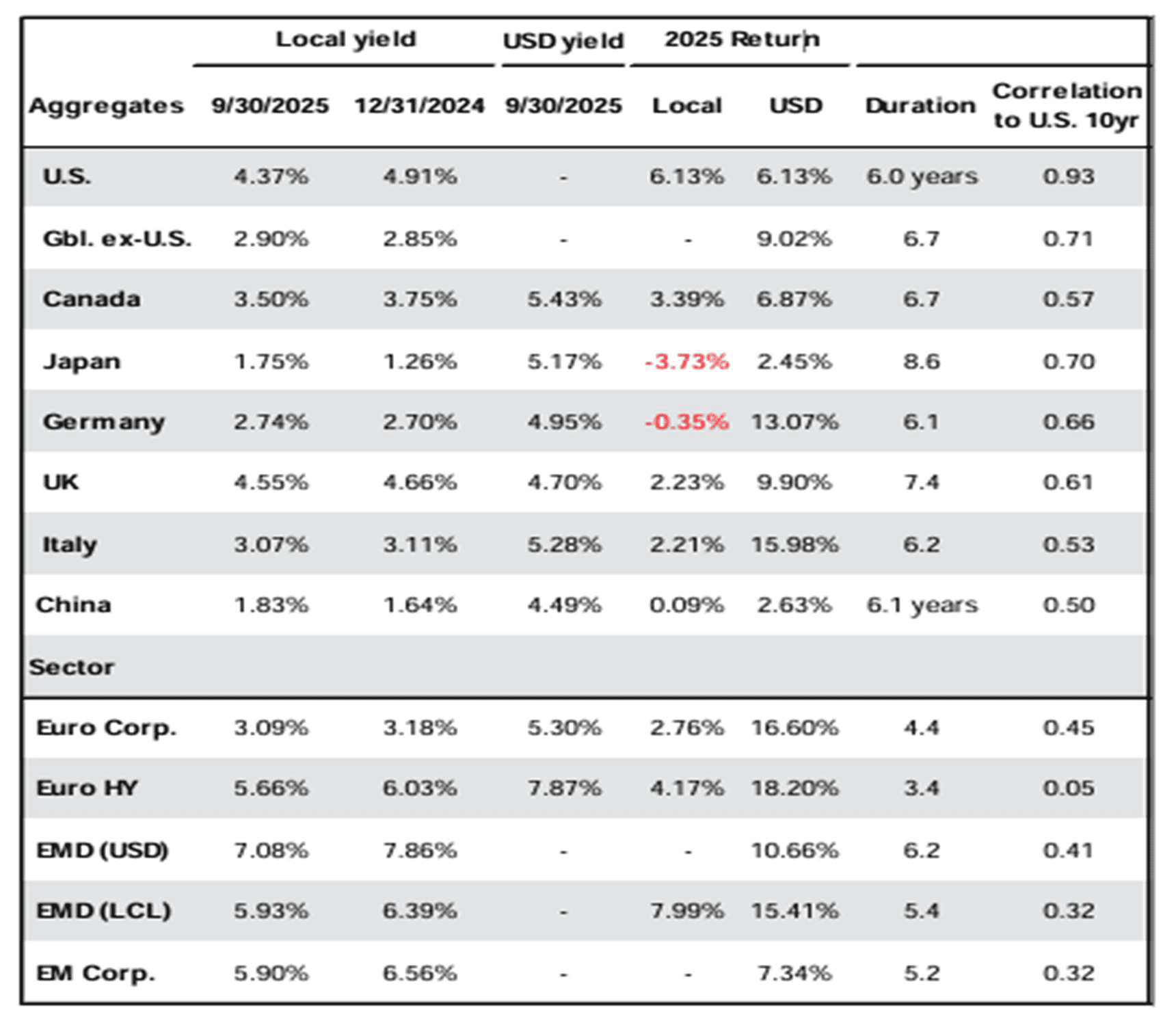

2025 Review: US Treasury yields faced pres-sure due to inflation and uncertainty stem-ming from tariff policies. Despite rate cuts by the Fed (which reached 3.50%–3.75% by year-end), long-term yields remained rela-tively high. In Europe, the Eurozone sover-eign bond index recorded a marginal positive return (approximately 0.4%–0.9%), impacted by the political crisis in France and concerns over its public debt. In Greece, Greek bonds continued to attract international investor in-terest, benefiting from the country’s improved credit rating and the convergence of spreads with the European core.

Source: JPMorgan – A Guide to the Markets

Forecasts for 2026 indicate that 10-year bond yields will move higher. UBS estimates that the US 10-year Treasury could reach 5.5% by late 2026, while J.P. Morgan projects levels around 4.35% for the US and 2.75% for the German Bund. In Europe, a significant in-crease in sovereign debt issuance is expected (near €1.4 trillion), primarily from Germany and France, due to fiscal deficits and defense spending. French yields remain particularly attractive, a fact clearly attributed to political uncertainty, with at least three prime minis-ters having held office without remaining for the last 18 months.

Investors are pivoting toward intermediate-term, high-quality (investment grade) bonds to ‘lock in’ yields before potential further rate cuts, while remaining cautious regarding low-rated corporate bonds (high yield) due to in-creased default risks. The Hellenic Republic plans bond issuances of up to €8 billion for 2026, with international rating agencies re-maining optimistic about further upgrades.

In summary, in 2026, the bond market will be required to balance government borrowing needs with the gradual normalization of cen-tral bank monetary policies.

Πηγή: JPMorgan – A Guide to the Markets

-

Alternative Investments

Alternative investments provided significant diversification in a highly volatile environ-ment in 2025, while the outlook for 2026 ap-pears positive, with an emphasis on deal ac-tivity recovery and new technologies. Hedge funds recorded positive results across all ma-jor strategies (such as equity long/short and macro), helping to mitigate losses during pe-riods of market instability.

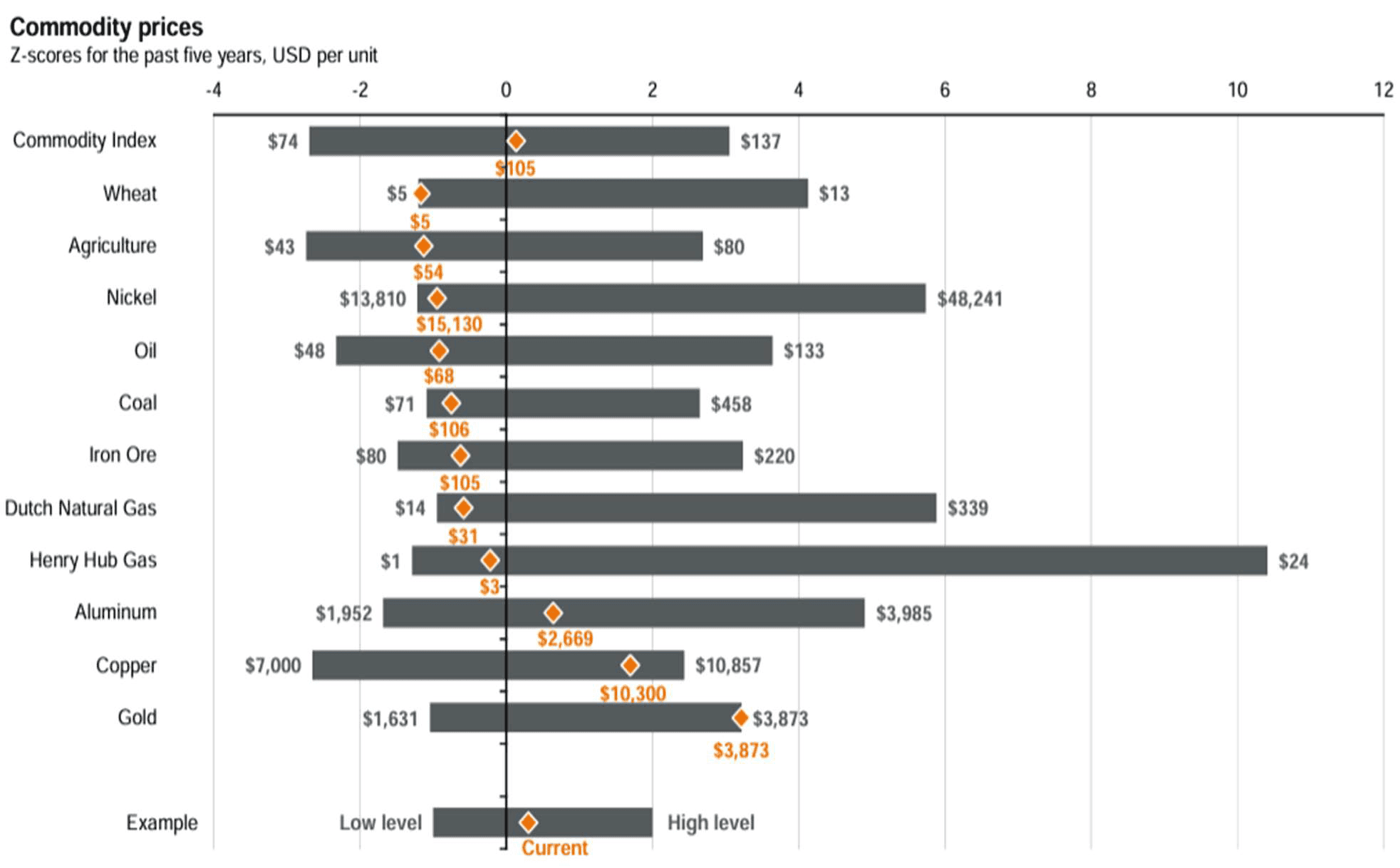

Private credit emerged as a frontrunner as banks tightened lending. This market ap-proached $2.5 trillion, offering attractive yields to investors. Gold delivered an excep-tional performance in 2025, surpassing the $4,000 milestone, supported by central bank purchases and geopolitical uncertainty.Despite the recovery in IPO activity (a 64.5% increase through October), capital raises re-mained at lower levels compared to previous years.

Source: JPMorgan – A Guide to the Markets

2026 is expected to be a strong year for exits and capital distributions in Private Equity, as declining interest rates lower financing costs and facilitate acquisitions. Artificial Intelli-gence (AI) and the energy transition will serve as the primary growth drivers. J.P. Morgan projects that infrastructure invest-ments will be bolstered by the demand for data centers and green energy. Further growth is anticipated in the secondary market (secondaries), as investors seek liquidity and ways to manage their portfolios within exist-ing private funds.

The Real Estate sector is entering a new cy-cle, with residential properties, logistics (warehouses), and specialized assets (such as data centers and life science centers) offering the best opportunities. According to J.P. Mor-gan, Private Equity is expected to deliver the highest returns among alternatives in 2026 (approximately 10.3%), followed by Real Es-tate (8%) and Direct Lending (7.6%).

In 2026, alternative investments will reward selectivity and discipline, acting as a ‘shield’ against inflation and the volatility of traditional markets.

Source: JPMorgan – A Guide to the Markets

-

Cryptocurrencies

The cryptocurrency market in 2025 was marked by sharp contrasts, moving from eu-phoria to “institutional maturation” with 2026 anticipated as a year of stabilization and inte-gration into traditional finance. Bitcoin peaked near $126,000 in October 2025 before falling below $93,000 in the fourth quarter due to macroeconomic pressures.

The return of Donald Trump boosted the market with a pro-crypto stance, including promoting a Strategic Bitcoin Reserve and rejecting CBDCs. Spot Bitcoin and Ethereum ETFs saw significant inflows, exceeding $57 billion for Bitcoin.

In 2025, Europe fully implemented the MiCA regulation, while the US introduced the GE-NIUS Act for stablecoins, requiring 100% re-serve backing. Professional translations using CoinDesk and Bloomberg Crypto terminology are provided.

-

2026 Outlook

The outlook for the global economy and mar-kets in 2026 is characterized by cautious op-timism and a return to more normalized con-ditions, although geopolitical uncertainty and trade tensions remain significant risk factors.

Key Trends for 2026:

-

Global Economy: Soft Growth

- US Slowdown: Following a strong trajectory in 2025, the US economy is expected to decelerate slightly, with growth moving near 1.5%-2%, as the impact of tariffs and higher interest rates becomes more pronounced.

- EU and Eurozone: Expected to maintain steady growth rates around 1.2%-1.4%, with domestic consumption recovering due to higher real wages.

- Emerging Economies: Led by Chi-na and India, these markets will re-main theprimary source of global growth, pro-jected at 4.1%. Forecasts indicating that China may surpass the US by 2030-32 align with this trend.

-

Monetary Policy: End of Tightening

- Further inflation de-escalation is ex-pected, giving central banks (Federal Reserve, ECB, Bank of England) the ‘green light’ for additional gradual rate cuts. The Bank of Japan (BoJ) will continue its policy normalization, rais-ing rates toward 1%.

- The falling interest rate environment favors the bond market, though high sovereign debt supply (due to in-creased fiscal spending, e.g., on de-fense) will keep yields at relatively at-tractive levels.

-

Equity Markets: Selectivity and Technology

- Following the strong performance of 2025, equity market returns are ex-pected to be more moderate in 2026.

- Investments in cutting-edge technolo-gies, such as Artificial Intelligence (AI), cybersecurity, and green energy, are expected to lead.

- As interest rates normalize, investors may pivot more toward ‘value’ stocks and less toward ‘growth’ stocks.

-

Alternative Investments & Cryptocurrencies

- An increase in private market activity (M&As) is expected, with private cred-it maintaining its momentum.

- The cryptocurrency market is expected to further integrate into the traditional system (via ETFs), focusing on utility (L2s, RWA tokenization), with prices increasingly dependent on macroeco-nomic conditions.

-

Source: OECD, Caldara, et al.

In 2026, the economy is moving toward a del-icate balance between demand recovery, the management of trade frictions, and the re-balancing of fiscal policies.

Source: JPMorgan – A Guide to the Markets

Disclaimer – Disclosures: This document is for informational purposes only, has been prepared by GWLAM, and does not constitute an offer, investment advice, or a solicitation of any purchase of investment products and/or any brokerage transactions or services. This letter is sent solely for information purposes, is personal, intended only for the named recipient, and may be used only by the recipient for this purpose. Neither this document nor any part of its content may be reproduced or distributed for any purpose without the prior written consent of GWLAM. While certain information has been obtained from published sources deemed reliable, no guarantee is given regarding its accuracy or completeness. Opinions, forecasts, assumptions, calculations, estimates, and target prices contained in this letter are valid as of the date of issuance and are subject to change at any time without notice. Specifically, cited pric-es, rates, and values do not constitute an indication that any investment can be performed at these prices. Conse-quently, GWLAM shall not be held liable for any direct, indirect, special, incidental, or consequential damages, includ-ing loss of profits, resulting in any way from the information contained in this letter. Past performance is not indicative of future results.