Newsletter March 2026

Economic Developments and Outlook

| First Quarter 2026 | Q1 2026 ended with the global macro regime shifting from disinflation + expected easing toward an energy-shock and stagflation-risk backdrop. |

| Investment signal | Stay selective: shorter-duration fixed income, quality equities, disciplined commodity hedges and a tactical rather than aggressive approach to crypto. |

In Brief

- The late-quarter Middle East shock changed the market message from ‘how fast will rates be cut?’ to ‘how much inflation pressure will energy create, and how long will it keep policy restrictive?’

- In the United States, inflation had cooled into February, with headline CPI at 2.4% and core CPI at 2.5%, but those readings pre-date most of the March oil spike and likely understate the new cost pressure entering fuel, transport and supply chains.

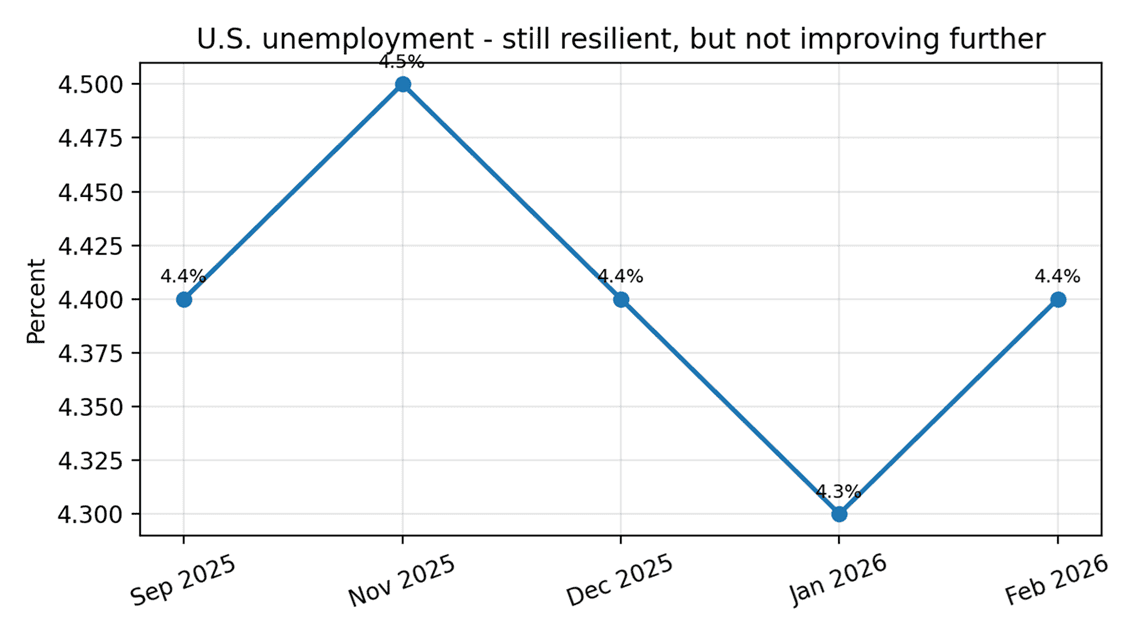

- The labor market has softened only gradually. U.S. unemployment was 4.4% in February, which is weaker than last year but not recessionary enough to force quick rate relief.

- Markets ended Q1 in a risk-off regime: oil surged, Treasury yields repriced higher, the Nasdaq entered correction territory, and the S&P 500 and Nasdaq were down 7.0% and 9.9% year-to-date respectively by March 27.

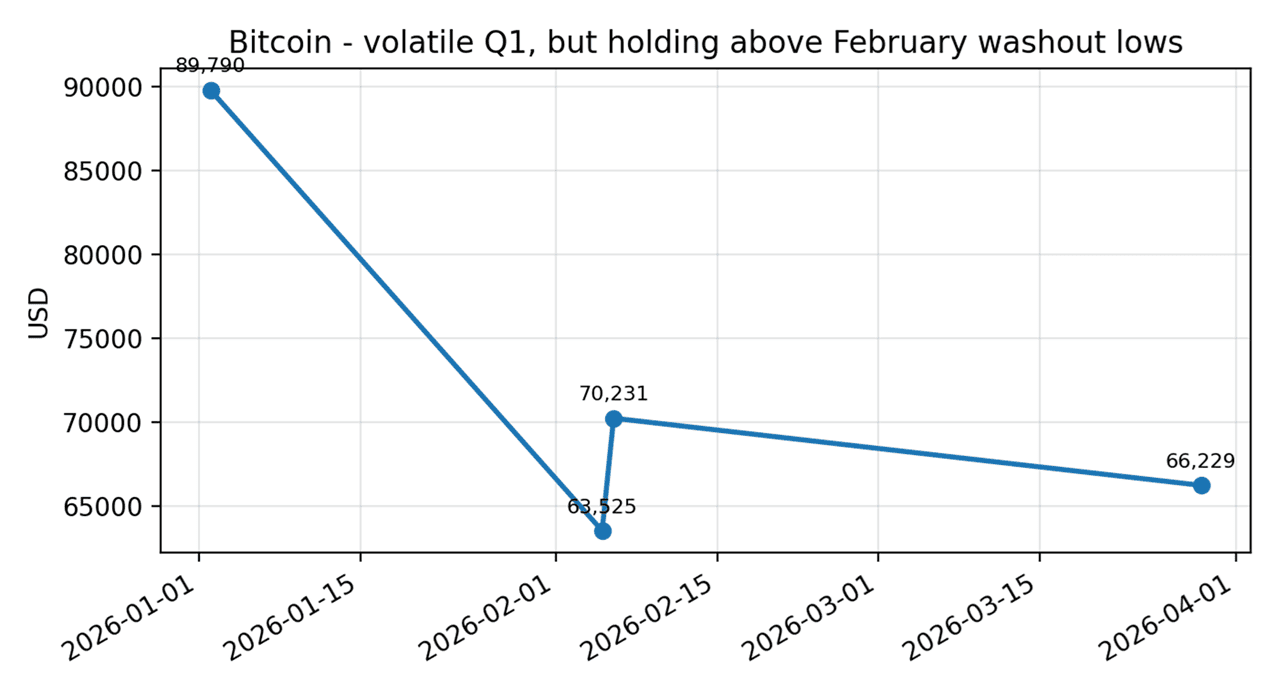

- Crypto remained a high-beta expression of macro risk appetite: Bitcoin held far above its February washout low, but institutional flows slowed after the Fed was interpreted as delivering a hawkish pause.

1. Macro Backdrop and Developments

The quarter opened with a constructive growth backdrop – resilient services, AI-linked capital spending and easing inflation – but ended with a geopolitical energy shock that materially worsened the inflation-growth trade-off.

The OECD’s March 2026 interim outlook kept global GDP growth at 2.9% for 2026 on the assumption that energy disruptions ease from mid-year, but it also warned that the conflict in the Middle East is raising costs, weighing on demand and adding inflation pressure.

That means the base case is still growth rather than outright global recession, but the confidence interval is much wider and much more dependent on the trajectory of oil, gas and shipping disruptions.

2. Interest Rates: Fewer Cuts, Higher Volatility

The most important market consequence of Q1 was the repricing of the interest-rate path.

The Federal Reserve left the target range unchanged at 3.50%-3.75% on March 18. By quarter-end, markets were increasingly treating that meeting as a hawkish pause rather than a prelude to near-term easing.

The bond market absorbed the change quickly. The U.S. 10-year Treasury yield rose from 4.191% on January 2 to 4.415% on March 26 and around 4.439% by March 29, as oil-driven inflation fears, weak Treasury auction demand and war-risk premia pushed term yields higher.

In Europe, the same shock made the ECB more cautious. Euro-area headline inflation is now projected by ECB staff at 2.6% for 2026, up from 2.1% in 2025, before easing back toward target in 2027.

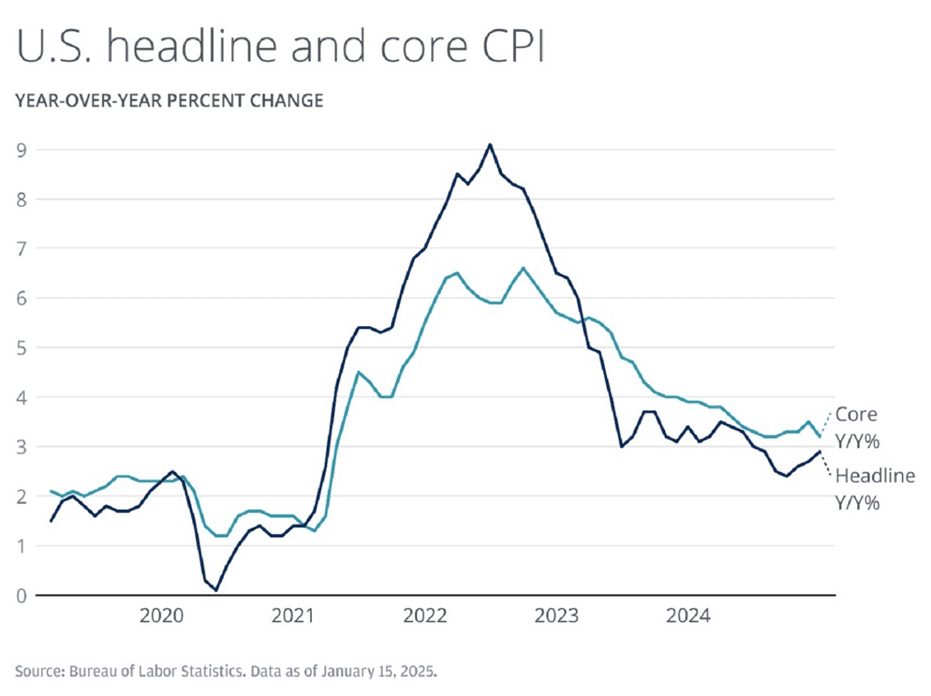

3. Inflation: Cooling before March, then re-risked by Energy

Incoming inflation data still looked encouraging through February, but they are now backward-looking relative to the March shock.

In the U.S., headline CPI was 2.7% in December 2025 and 2.4% in both January and February 2026; core CPI eased from 2.6% in December to 2.5% in January and February.

In the euro area, headline HICP fell to 1.7% in January before rebounding to 1.9% in February, while HICP excluding energy remained firmer at 2.4% in February. The message is clear: disinflation had progressed, but core/services pressure had not fully disappeared even before oil spiked.

4. Labor Market: Softer, but still not weak enough to dominate policy

The labor market did cool, but not in a way that offset inflation concerns.

U.S. unemployment was 4.5% in November 2025, 4.4% in December, 4.3% in January 2026 and 4.4% in February. This is consistent with a labor market that is no longer overheating but is still too resilient for policymakers to ignore inflation risks.

That matters because an energy-led inflation shock becomes especially difficult for central banks when the labor market is still reasonably intact: easing too early risks entrenching inflation expectations, but staying restrictive for longer increases the chance of a later growth and hiring slowdown.

Chart 5. U.S. unemployment drifted higher, then stabilized around 4.4%

BLS household survey data; October 2025 observations were unavailable because of the federal government shutdown.

5. Market Update: Equities, Dollar and Cross-Asset Positioning

By late March, markets were no longer pricing a clean soft-landing regime.

On January 2, the S&P 500 and Nasdaq stood at 6,858.47 and 23,235.63. By March 27 they had fallen to 6,368.85 and 20,948.36 respectively, leaving the indices down 7.0% and 9.9% for the year. The Nasdaq had entered correction territory.

Reuters described Q1 as a quarter in which geopolitics wiped roughly $7 trillion off global stocks, oil and gas prices surged, and the usual diversification benefits from gold and high-quality bonds became less reliable.

6. Crypto Market and Outlook

Crypto remained extremely sensitive to the same macro forces driving equities and rates, but it also showed relative resilience after the February liquidation event.

Bitcoin started the year near $89,790 on January 2, then fell to roughly $63,525 on February 5 in its sharpest one-day drop since November 2022, before rebounding above $70,000 on February 6. By March 29 it was trading around $66,229.

Institutional flow data suggest that the market is still attracting capital, but with more hesitation. CoinShares reported US$230 million of net inflows for the week of March 23, with strong flows early in the week followed by US$405 million of post-FOMC outflows as investors interpreted the Fed as more hawkish.

The crypto outlook for Q2 depends on three variables: first, whether energy-driven macro stress keeps real yields elevated; second, whether the Fed regains room to ease later in the year; and third, whether regulation remains supportive enough to sustain institutional participation. In the near term, crypto still behaves as a leveraged macro asset, not as a defensive haven.

Chart 7. Bitcoin: sharp February washout, partial recovery into quarter-end

Selected checkpoints from Reuters and current market data on Mar 29, 2026.

Investment Stance

- Fixed income: favor short-to-intermediate duration until inflation expectations stabilize.

- Equities: lean toward quality, cash-generation, pricing power and selective energy/defense exposure.

- Commodities and gold: useful as hedges, but gold’s short-run performance can still be hurt by a stronger dollar and higher real yields.

- Crypto: tactically constructive only if macro stress eases; otherwise expect volatility and sentiment-driven drawdowns.