Recovery Tracker: A Real-Time Look at the Post-Covid U.S. Economy

In a few short weeks, the coronavirus pandemic slammed the brakes on the U.S. economy, shuttering businesses and putting tens of millions out of work.

A U.S. recession is all but officially under way. The speed at which the economy has ground to a halt has rendered much of the traditional economic data — typically released with a lag of about a month — outdated before it’s even published.

To fill the gap, Bloomberg economists Eliza Winger and Tom Orlik created a weekly dashboard of high frequency, alternative and market-based indicators. Right now, the dashboard shows the depths of the downturn. In the weeks ahead — as states move toward re-opening — it should capture the strength of the recovery.

Several of the dashboard’s data points signal a deepening contraction, with further declines in consumer confidence and the number of active oil rigs. Others, like jobless claims, suggest the most extreme period of decline is now over, but remain extremely weak and support expectations for the economy to shrink this quarter by the most in records dating back to the 1940s.

Notes: Weekly new Covid-19 cases based on data from Bloomberg News and Johns Hopkins. Lockdown index from Oxford COVID-19 Government Response Tracker from zero to 100. Jobless claims in millions. Mortgage applications are percent changes from the average of the first two weeks in January. Public Transport Use from Moovit, (average of New York area, Chicago and Los Angeles). Restaurant bookings (%YoY) from OpenTable; Store sales (%YoY) from Johnson Redbook sales. Bloomberg Consumer Comfort index levels zero to 100; Oil rigs, steel production and S&P 500 are percent changes from the average of the first two weeks in January. Bloomberg Financial Conditions Index.

Source: Bloomberg Economics

“The high-frequency data paint a grim picture,” Winger and Orlik said. “Soaring jobless claims, empty restaurants, and a falling count for active oil rigs show the breadth and depth of the blow to the economy.”

Americans staying home for fear of transmitting the virus, along with government-ordered shutdowns aimed at protecting lives, have caused the economic downturn. That makes the number of new Covid-19 cases all the more important. That pace eased last week but it remains extremely elevated, and limited testing means the count almost certainly understates the true spread of the disease.

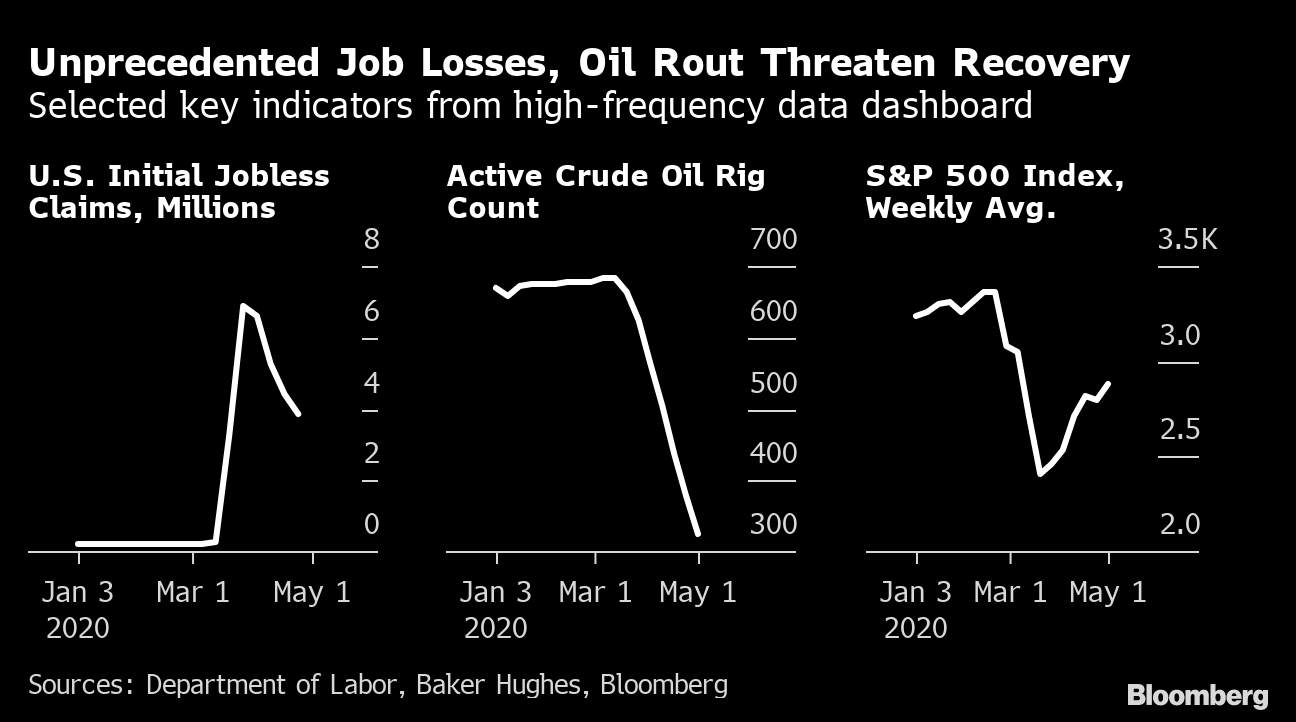

Filings for unemployment benefits (or initial jobless claims) remain extremely high but have fallen for four straight weeks — suggesting the breakneck pace of layoffs may be slowing. Unlike many government reports, jobless claims are reported with just a one-week lag. More than 30 million Americans filed for unemployment benefits since March 15, essentially wiping out all of the jobs created since the last recession.

The Bloomberg Consumer Comfort Index, a weekly confidence measure, has declined in 12 of the last 13 weeks. The measure has plummeted from 67.3 in the last week of January to 39.5, the steepest drop in more than three decades worth of data.

Crushed by the Saudi-Russia price war in March and government shutdowns that have kept Americans off the roads, oil prices have crumbled in recent weeks. The active oil rig count slumped 51% since the first two weeks of January, according to Baker Hughes data.

Unprecedented Job Losses, Oil Rout Threaten Recovery

Selected key indicators from high-frequency data dashboard

Sources: Department of Labor, Baker Hughes, Bloomberg

The housing market hasn’t been spared either: Home sales are already down and are expected to crater in the coming months. A more real-time indicator, mortgage applications for home purchases, has fallen 27% since the first two weeks of the year.

Data from OpenTable, a restaurant-booking app, offer insight into the devastating blow faced by the restaurant industry: Restaurant bookings have dropped 99% from last year. Restaurants in some states opened their doors to customers last week, supporting the barest improvement in the figure from a 100% decline.